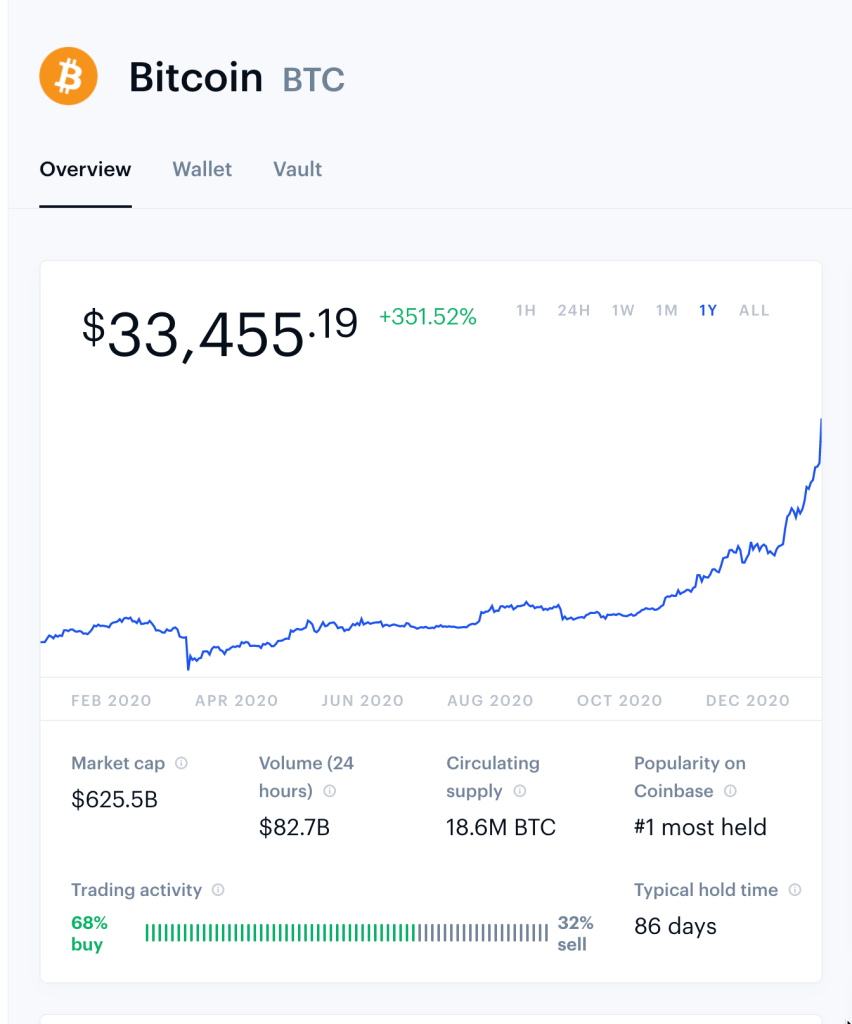

Bitcoin has increased by 300% in the last three months from $10k (Oct 3) to $33k per $BTC (Jan 3). Ethereum has also increased by 270% in the same period from $350 (Oct 3) to $950 (Jan 3) per $ETH.

I started buying Cryptocurrency in early 2013 ($BTC mainly) mainly because I thought it was an interesting concept at ~$50 a coin. I ‘lost’ most of these coins as part of the Mt Gox Bankruptcy in 2014. I’m hopeful that 10-15% of our holdings may be returned soon, after seven years of waiting.

The US government has printed more than 20% of the total USD in circulation in 2020 alone (over $USD 9 Trillion) and many people have no idea we just got a lot poorer. Given this is happening globally (across governments) I’m starting to think that I should have a more significant percentage of my savings in $BTC and cryptocurrency in general over fiat ($USD). There are also lots of other benefits/value of cryptocurrency beyond inflation protection but I won’t cover them here.

Ultimately, I’d like to allocate 10%+ in Crypto, 20% in technology companies (private), 30% in real estate and 40% in public equities (mostly in tax advantaged retirement and non liquid accounts) but this will take many years and a good amount of luck, too 🙂

Given these observations, here is how I’ll modify my strategy going forward.

Crypto Strategy

- Focus on $BTC and $ETH: Most of my $BTC is locked up in Mt. Gox (stuck in bankruptcy proceedings), and this counts towards my overall allocation. I assume around 15% of coins returned at some point as $BTC (not fiat). My next largest position is ETH which I’ve had for years. I plan to hold BTC/ETH/All Altcoins in a 50/35/15 ratio in terms of USD fiat value.

- Regular Purchase: I started taking 15% of my paycheck (2x per month) and purchasing $BTC and $ETC in an equal ratio (50/50) as I am over indexed in $BTC. The goal here is to remove emotion from the decision and dollar cost average over the next few years.

- Crypto Savings Account: I moved all my extra money to BlockFi and now Celsius (referral links). I have kept some $BTC and $USDC (USD stablecoin) in BlockFi the last year and would rather make 5-8% interest vs. 0.5% interest in traditional finance alternatives. Note that BlockFi is not risk free (they are investing your capital and lending just like banks, but without FDIC insurance) but they do have strong security measures to protect your collateral.

- (optional) DeFi: I have positions in all the stuff powering Decentralized Finance (DeFi) on the Ethereum network, which started for fun but now is more significant (which is how $BTC started for me anyway). I play around with staking, liquidity pools and lending but beware the gas fees (I got burned). My largest position outside of ETH is in this DeFi Pulse Index (https://defipulse.com/blog/defi-pulse-index/) which is a weighted index of all the tokens powering DeFi.

I also hold small amounts of other Altcoins like Stellar Lumens ($XLM), Polkadot ($DOT), Ripple ($XRP), Filecoin ($FIL bought in the 2017 SAFT), Arweave ($AR), UNI ($UNI), Sushi ($SUSHI), Cosmos ($ATOM), Solana ($SOL) as well as about a dozen others, but those are more out of interest than part of an actual strategy. I also added NFTX as an index for collectibles to the mix.

All of this is still very experimental, and I wrote this up to share more easily and get feedback. Despite dabbling for eight years, I still feel like a n00b most of the time in the crypto world.

Leave a comment